One of the most common mistakes I see buyers make before they ever look at a single financial statement is assuming that an RV park is an RV park. They find a listing, they like the location, they request the financials, and they start running numbers without ever stopping to ask a more fundamental question.

What kind of park is this, and does that match what I am trying to buy?

It sounds basic. It is not. The type of park you are buying determines your revenue model, your financing options, your operational complexity, your guest profile, your risk exposure, and ultimately your returns. Getting clear on park type before you underwrite a deal is not a detail. It is the foundation.

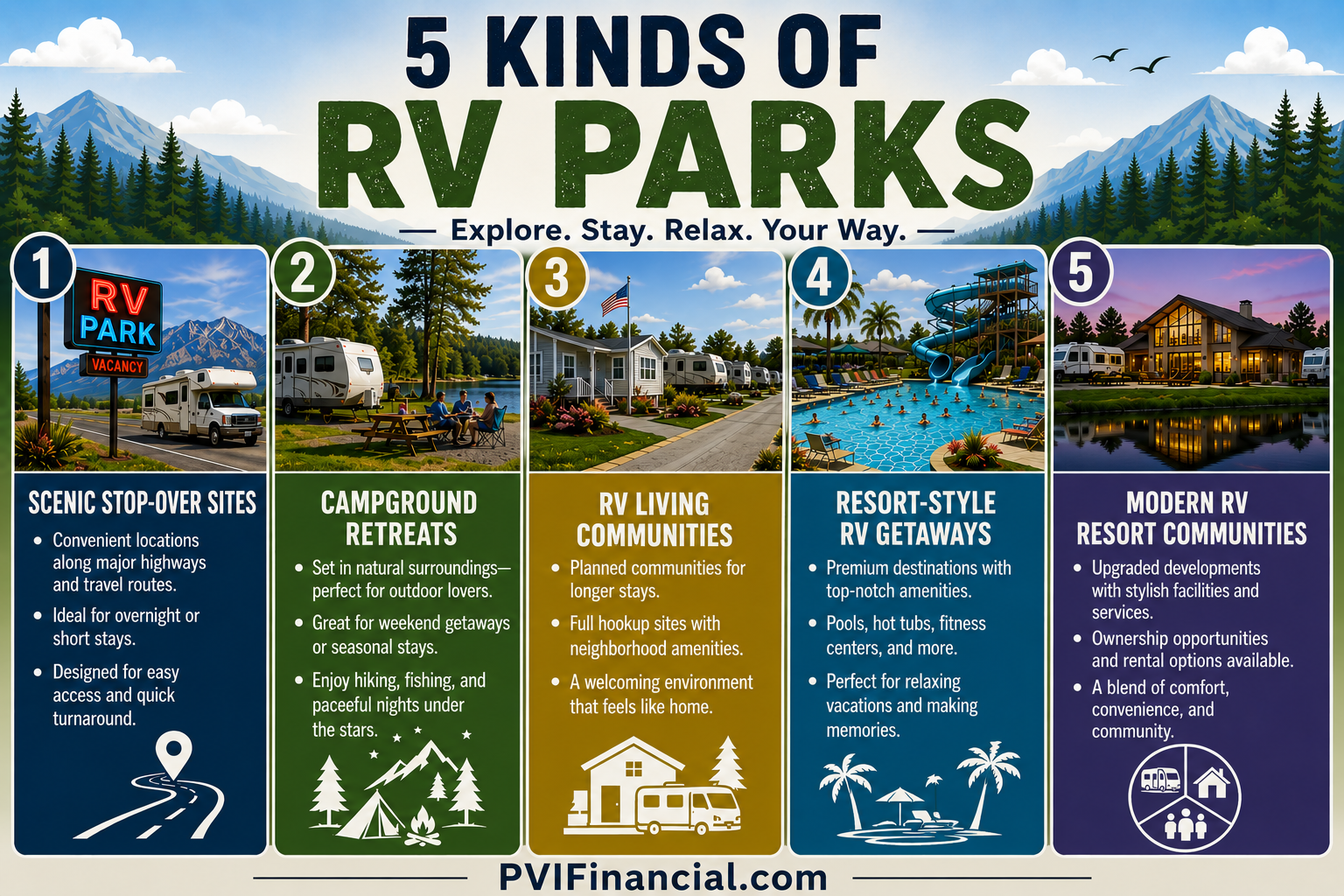

There are five distinct types of RV parks, and each one operates as a fundamentally different business.

1. Roadside RV Parks

These are the highway corridor stops, the parks that exist because a traveler needs to sleep somewhere between Point A and Point B. Guests stay one to two nights and move on. There is no loyalty, no repeat booking relationship, and no reason for the guest to choose your park specifically over the one three exits down except convenience and availability.

From an investor standpoint, roadside parks are the most traffic-dependent and the most volatile. A new highway bypass, a competing park with better online reviews, or a slow travel season can all hit occupancy hard and fast. They can work as investments but they require the right price, the right location, and a clear-eyed view of the demand drivers before you commit.

2. RV Park Campgrounds

Typically located one to two hours outside a metro area, these parks benefit from tourism demand, nearby outdoor recreation, lakes, trails, state parks, and the kind of destination that draws weekend and week-long travelers. Guests are not just passing through. They chose this area.

These parks tend to have stronger repeat guest potential than roadside parks and benefit from the growing demand for outdoor recreation experiences. They are also more sensitive to seasonal patterns, so monthly cash flow modeling matters significantly when you are underwriting one of these.

3. RV Park Communities

Long-term stay communities where residents live on-site full time or for extended periods. The revenue profile looks more like a mobile home park than a hospitality business, predictable monthly income from a stable tenant base with low turnover.

The tradeoff is rate. Long-term tenants pay significantly less per night than transient guests, and as I have written about before, a heavy concentration of long-term tenant revenue can create real financing challenges with SBA and conventional lenders who classify that income as residential rather than commercial. If you are buying a community-style park, understand the financing implications before you go under contract.

4. RV Park Resorts

The premium tier. These parks compete on amenities and experience, pools, water slides, clubhouses, entertainment, the full resort package. Guests come specifically because of what the park offers, not just where it is located. Premium nightly rates are possible and repeat guest loyalty can be very strong.

The operational overhead is higher, the amenity capital requirements are real, and the management complexity is greater than any other park type. These are not beginner acquisitions. But for an experienced operator with the capital and the team to run them well, the return profile can be exceptional.

5. Hybrid RV Parks

The newest and most complex category. Hybrid parks combine multiple revenue models, sometimes including fractional ownership or timeshare-style interests alongside traditional site rentals. The revenue diversification can be attractive but the legal and operational complexity is genuinely significant.

If you are evaluating a hybrid park, make sure you have both a real estate attorney and a CFO in your corner before you go far down the road. The structures vary widely and the due diligence required goes well beyond what a standard park acquisition demands.

Why This Matters for Your Underwriting

Every number in a park’s financials means something different depending on the park type. A 70 percent occupancy rate at a roadside park tells a very different story than a 70 percent occupancy rate at a destination campground. A strong T12 at a resort park built on amenity-driven demand is a different asset than a strong T12 at a community park built on long-term tenant stability.

When I underwrite a park deal for a client, the first thing I want to understand is not the revenue number. It is the revenue model. What type of park is this, who is the guest, why do they come, and what happens to occupancy if one of those drivers changes?

The type determines the risk. The risk determines the price.

The Bottom Line

Before you request financials on your next deal, ask yourself what type of park you are actually looking at. Each model has different risks, different rewards, and a different operational reality once you own it. Knowing the difference before you make an offer is not optional. It is the starting point for every other analysis you are going to do.

If you want help figuring out what type of park you are evaluating and whether the numbers support the price being asked, that is exactly what I do at pvifinancial.com.

And if you have not grabbed a copy of my book yet, From Offer to Operation: The Complete RV Park Investor’s Guide ($49), it covers the full acquisition and operations framework including a bonus report with 34 red flags to verify before you close. I am very confident you will learn something you had not thought of.

You can get it direct here: https://wendipvifinancial.gumroad.com/l/kqmyb

Or if you prefer Amazon has it too, just search author Wendi Rook.

~Wendi | Fractional CFO | PVIFinancial.com

Click here to read “The Sellers Proforma is Not Your Proforma” next

Leave a Reply