If you are trying to figure out how to buy an RV park in a competitive market, you are not alone, and the competition is real. The outdoor hospitality space has exploded in popularity, and the supply of quality parks for sale has not come close to keeping up with demand. Good deals get multiple offers. Sellers know their leverage. And buyers who are not prepared move slow, lose deals, and wonder what happened.

Here is what serious buyers who know how to buy an RV park in a competitive market do differently.

How to Buy an RV Park in a Competitive Market: 7 Moves That Win Deals

1. You have to be underwritten before you make an offer

This is the single biggest mistake I see new investors make. They fall in love with a deal, make an offer, and then start running the numbers. By the time they figure out what the deal is actually worth, the seller has already accepted someone else’s offer or the LOI window has closed.

Understanding how to buy an RV park in a competitive market starts with having your numbers ready before you fall in love with a deal. That means looking at the trailing 12 months of revenue and expenses, stress-testing occupancy, modeling your financing, and building a real NOI picture, not the one the broker handed you. You need to know your max price before you enter a negotiation, not after. If you want to understand what that rebuild actually looks like, start with What is NOI? And How to Find the REAL Number in an Acquisition.

This is the foundation of how to buy an RV park in a competitive market and the step most buyers skip entirely.

2. Fast underwriting is a competitive advantage

Most buyers take a week or two to run their numbers. If you can turn a full underwrite in 24 hours, you show up to every deal faster and more credible than the competition. Speed and accuracy are the two things that define how to buy an RV park in a competitive market successfully.

This is exactly where working with a Fractional CFO who specializes in RV park acquisitions changes the game. I offer deal underwriting as a standalone service for buyers who need speed and accuracy. You send me the financials, I build the model, and you have a decision-quality analysis often within 24 hours. You know your offer price, your cap rate, your cash-on-cash return, and your risk flags before you ever pick up the phone with the broker. Deal screening starts at $500 and a full acquisition underwrite runs $750 to $1,500 depending on complexity. You can see the full breakdown at PVIFinancial.com.

That is how you buy an RV park in a competitive market and actually win.

3. Stop relying on the broker’s numbers

Brokers represent sellers. The OM they hand you is built to make the deal look as good as possible. Expense ratios are often understated. Vacancy assumptions are optimistic. Revenue projections include upside that may or may not materialize.

Your job is to recast those numbers based on reality. That means using actual industry expense ratios, realistic occupancy by season, market rate comparisons for the area, and your own financing assumptions. I covered exactly how this plays out in The $312,000 Mistake: What Happens When a Buyer Accepts the Seller’s NOI Without Rebuilding It. If the deal still works after your recast, you have something worth pursuing. If it only works using the broker’s numbers, walk away.

This is one of the most important things to understand about how to buy an RV park in a competitive market.

4. Know what you’re actually buying

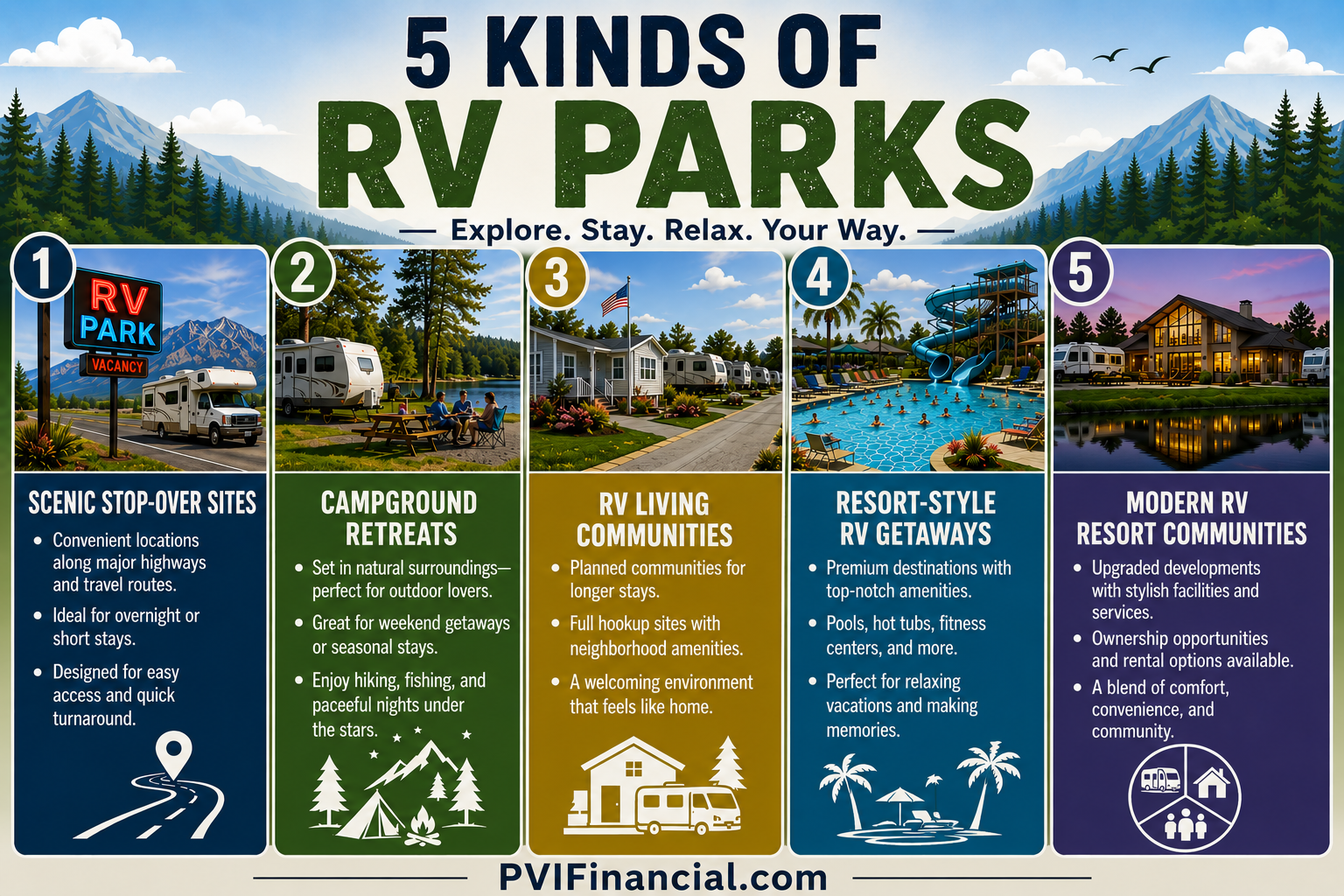

An RV park is a business, not just a piece of real estate. The land matters, but so does the revenue mix, the customer base, the online reputation, the utility infrastructure, the age of hookups, the permit status, and a dozen other operational factors that do not show up on a cap rate summary.

Before you get too deep into any deal, make sure you understand where the revenue actually comes from. Is it seasonal or year-round? Is it heavily OTA-dependent? Are there long-term tenants subsidizing the numbers in ways that inflate NOI but limit upside? How old are the electrical pedestals? These are not afterthoughts, they are part of the underwriting. The Due Diligence Items Nobody Talks About is a good place to start, and so is Before You Fall in Love With That RV Park, Do This First.

5. Get your financing pre-organized

Competitive sellers favor buyers who can close. If you show up to a deal still figuring out how you are going to finance it, you are already behind. Know your lender before you need them. Understand whether your deal is SBA-eligible or conventional. Have a conversation with a lender who specializes in outdoor hospitality before you are under contract so you know your parameters going in.

A pre-organized buyer moves faster and negotiates stronger. If you want to understand what lenders are actually looking at when they evaluate a deal, read What a Lender Actually Looks at Before Approving an RV Park Loan.

Buyers who know how to buy an RV park in a competitive market show up with their financing already figured out.

6. Build relationships with brokers before you need them

The best deals in outdoor hospitality do not always make it to LoopNet. Brokers who work this niche have buyers lists and they call their trusted buyers first. If you are not on those lists, you are competing over whatever is left.

That means proactively reaching out to brokers who specialize in RV parks and campgrounds, telling them exactly what you are looking for, and following up consistently. Be someone they want to call.

Building broker relationships before you need them is one of the most underrated strategies for how to buy an RV park in a competitive market.

7. Make clean offers

One of the most overlooked aspects of how to buy an RV park in a competitive market is how you present yourself as a buyer. Know your price, know your contingency timeline, and do not load up the LOI with unnecessary complexity. Sellers who have multiple offers on the table are going to choose the buyer who looks the most capable of closing, not necessarily the one with the highest price.

A clean, well-structured offer from a credible, prepared buyer beats a messy high offer more often than people think.

One more thing most buyers never think about until it is too late: how you present yourself financially matters as much as the offer itself. A seller with multiple LOIs on the table is going to feel more confident in the buyer whose personal financial statement is clean, current, and organized, not the one who scrambles to email over a blurry PDF at the last minute.

I offer personal financial statement review and packaging as part of my acquisition support services. I will look at what you have, identify anything that could give a seller or lender pause, and help you put together a buyer package that signals you are serious, qualified, and ready to close. It is one of those things that costs very little and can absolutely be the difference in a competitive situation.

If you want help getting your financials buyer-ready, reach out at PVIFinancial.com.

The bottom line

Knowing how to buy an RV park in a competitive market is not impossible, but it is not easy either. The investors who are winning deals are the ones who are prepared before the opportunity shows up, not scrambling to get ready after it does.

If you want help on the financial side of your next acquisition, from underwriting to deal structure to understanding what the numbers are really telling you, that is exactly what I do. Reach out at PVIFinancial.com and let’s talk about your deal.

~Wendi | Fractional CFO | PVIFinancial.com